OUR SUMMARY

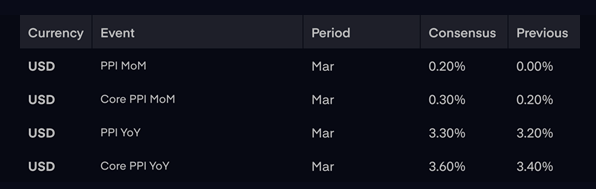

The U.S. dollar continues to face pressure amid a confluence of weakening investor confidence and shifting capital flows toward traditional safe havens such as the Swiss franc, euro, and Japanese yen. A subdued U.S. CPI print further accelerated the dollar’s decline, reinforcing dovish sentiment. However, any meaningful rebound in the greenback would likely require a significantly stronger-than-expected PPI reading to reignite demand.

From a technical standpoint, CHF, EUR, and JPY appear overbought relative to USD, suggesting a possible correction could be near. Still, without a clear catalyst—such as a resurgence of confidence in U.S. fundamentals—such a correction may struggle to gain momentum.

In the UK, economic data provided a rare upside surprise. February GDP rose 0.5%, significantly above the 0.1% consensus forecast. Strong performances in both the manufacturing (+2.2%) and services (+0.3%) sectors contributed to the beat. Despite this, gains in GBP remained subdued, reflecting lingering caution in the broader outlook as the Office for Budget Responsibility has cut its growth forecast for the year by half.

Turning to the euro, its role in investor portfolios appears to be shifting. Traditionally treated as a risk-on currency, the euro is now benefiting from safe-haven inflows. Contributing to this shift are recent moves from Germany toward growth-friendly fiscal policy and the EU’s measured approach in delaying retaliatory tariffs on the U.S.—moves that have positioned Europe as a source of stability. While EUR strength has coincided with broad USD weakness, there are emerging signs that the single currency may be asserting itself more independently.

With EURUSD and the broader euro index at multi-year highs and technical signaling overextension, a pullback may be due. However, without a decisive shift in sentiment or fundamentals, the euro’s upward trajectory may still find support in its evolving role and relative macro stability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}